Les actualités de la BRVM en Flux RSS

Les actualités de la BRVM en Flux RSS

Nous agrégeons les sources d’informations financières spécifiques Régionales et Internationales. Info Générale, Economique, Marchés Forex-Comodities- Actions-Obligataires-Taux, Vieille règlementaire etc.

Enjoy a simplified experience

Find all the economic and financial information on our Orishas Direct application to download on Play StoreGlobally, stock markets have once again proven that they are the best reflections of economic developments. Remember that the stock price of a company is the fairest value that results from supply and demand and that best reflects investors' expectations about the financial health of the company concerned by taking into account macroeconomic data (GDP growth, inflation rate, exchange rate, etc.) as well as those of the company itself (turnover, profit, dividends, financial perspectives, etc.). The stock market indices on which attention has been so focused in recent days in the midst of the Coronavirus (COVID-19) pandemic, constitute the best synthesis of the health of a country's economy; as it should be noted that they are generally made up of a sample of enterprises that come from various sectors of economic activity and that are sufficiently representative of the economy as a whole. Thus, by looking at the behavior of the index, we can deduce the direction in which the economy is oriented. It is for these different reasons that the stock markets, through prices and indices, have been scrutinized lately because they give the best expectations on the evolution of the global economy in the face of COVID-19.

Impact on the global economy

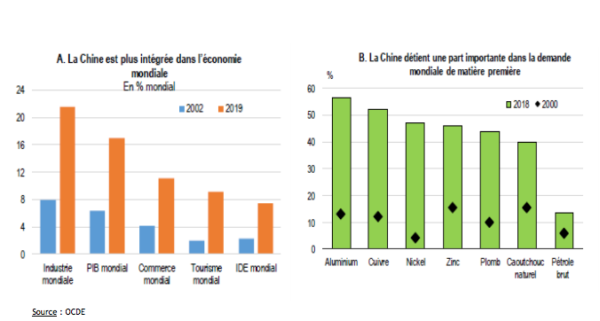

According to the OECD1, the COVID-19 pandemic would lead to a large-scale contraction in Chinese production. Thus, China's growth would fall below the 5% mark in 2020 against 6.1% in 2019, before rising to more than 6% in 2021; when production will gradually return to the levels expected before the arrival of the epidemic. Due to China's strong integration into global activity, a contraction in its economy would negatively impact global growth, due to the direct disruption of the world's supply chains from China2 , the weakening of China's final demand for goods and services3 , as well as the decline in tourist flows4 . According to a study published on February 11, 2020 by the Oxford Economics Institute, global tourism revenues are expected to fall by at least $22 billion, following the most optimistic scenario assuming a 7% drop in travel abroad by Chinese. The shortfall could reach $49 billion (€44.6 billion) if the crisis lasted as long as the 2003 SARS5 crisis and $73 billion (€66.5 billion) if it lasted longer.

China, the workshop of the world, but also its pharmacy.

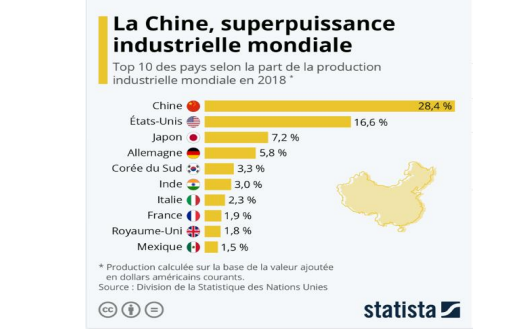

According to the United Nations, China is now the world's leading industrial power and plant closures in the country are already causing supply problems for many companies around the world.

China, the world's leading industrial power ahead of the USA.

At the global level, under the assumption that the epidemic peak would be reached in China in the first quarter of 2020 and that in other countries it will prove to be more moderate and circumscribed, global growth, according to the OECD, would slow to 2.4% in 2020 against 2.9% in 2019. This development reveals a contrasting situation across the regions. Indeed, the effects of the coronavirus outbreak are expected to be limited in the United States and Canada, although loss of confidence, disruptions in supply chains and weaker external demand will dampen growth prospects. Growth rates are expected to increase from 2.3% in 2019 to 1.9% in 2020 for the US and from 1.5% to 1.3% for Canada.

In the euro area, growth is expected to average around 1% per year over 2020-21 compared to 1.2% in 2019. The decline is amplified by the situations of confinement imposed in some European states, especially in Italy. In the United Kingdom, the GDP growth rate is expected to be 0,8 % in 2020 compared to 1,3 % in 2019 (6) . In emerging economies, a gradual but modest recovery is expected for 2020-21, however the extent of this recovery is uncertain, given the Coronavirus (COVID-19) epidemic. According to the OECD, an upward reorientation would presuppose a positive impact of the reforms carried out, an accompanying monetary policy in India and Brazil, well-targeted measures in Mexico and Turkey to stimulate sustainable growth, and a gradual recovery in the activity of commodity-exporting countries exposed to the likely slowdown in the Chinese economy. Thus, in Mexico growth is expected to remain at 0.7% in 2020 against 0.7% in 2019 and in Turkey, GDP growth would be 2.7% in 2020 against 0.9% in 2019.

In Africa, economies' dependence on commodity exports, particularly to China, makes them particularly vulnerable to a likely contraction of the Chinese economy. Indeed, for more than two (2) decades, trade links between Africa and China have continued to grow. In 1996, China was the largest source of imports for a single African country: The Gambia. Nearly 20 years later, 24 African countries are now for which the Asian giant represents the world's leading supplier of goods. Moreover, according to the Chinese Ministry of Agriculture and Rural Affairs, the volume of trade in agricultural products between China and Africa increased tenfold between 2000 and 2018. Trade volume increased from $650 million in 2000 to $6.92 billion in 2018, recording an average annual growth of 14%.

At the WAEMU level, the Coronavirus epidemic could impact the Union's growth in connection with the decline in exports and imports. Indeed, according to the BCEAO (7), 43.7% of the Union's exports of goods were destined for Europe, of which 25% for the European Union and 18.7% for the other countries of the continent. Switzerland, the Netherlands and France remain WAEMU's main customers, accounting for 17.5 per cent, 6.5 per cent and 5.8 per cent of exports respectively during the period under review. Thus, the quarantine of certain regions of Europe should lead to a decrease in demand from these areas, hence possibly a negative impact on the exports of WAEMU member states.

Regarding imports, the main sources of supply for WAEMU countries are the European Union (41.4%), Asia (35.7%), Africa (15%) and America (6.9%). Acquisitions of goods from Asia consist mainly of food products, mainly rice from Thailand and India, capital goods and intermediates, with relative shares of 29.8%, 30.7% and 20.7% respectively. Intermediate goods from Asia are delivered in particular by China (66.2%), India (10.1%) and Japan (6.8%). In the light of these statistics, the reduction of activities within the European Union and in China could deprive the Union of various intermediate goods, with a potential negative impact on the industrial sector.

MOREOVER, ACCORDING TO THE OECD, IN A SCENARIO OF DOMINO CONTAGION, WIDELY SPREAD AND DIFFICULT TO CONTROL, GLOBAL GROWTH WOULD DECLINE TO 1.5%. IN THIS CASE, CHINA WOULD FIRST BEAR MOST OF THE SLOWDOWN, WHICH WOULD THEN BE FELT IN ASIA, EUROPE AND NORTH AMERICA. TRADE WOULD ALSO BE "SIGNIFICANTLY LOWER", FALLING BY ABOUT 3% OVER THE YEAR AND AFFECTING THE EXPORTS OF ALL ECONOMIES. SOME NATIONS, ESPECIALLY IN THE EUROZONE, COULD ALSO ENTER RECESSION.

Financial market reaction

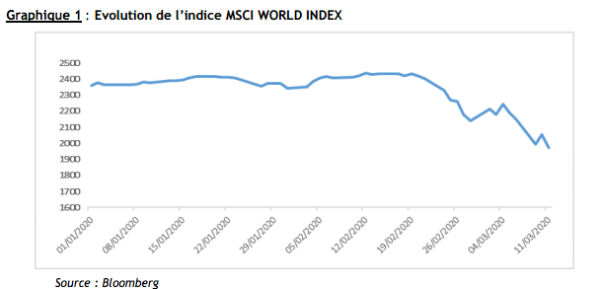

The anticipated slowdown in global economic growth induced by the epidemic is already reflected in the performance of the MSCI WORLD INDEX, an index representing the performance of stocks listed on twenty-three (23) stock exchanges from developed economies. Indeed, the index has lost 18% of its value since February.

All regions of the world seem to be caught up in this market correction. Indeed, while Asian markets were the first to be affected, China's position as the world's second-largest economy and its sprawling trade relations led to a wide spread of stress in the markets. The shock was all the more important as the financial markets of developed countries were coming out of more than ten (10) years of increase, driven by the accommodative monetary policies of central banks.

Thus, these markets seemed for some time immune to the very notion of risk, despite stock market multiples having reached very high levels. The COVID-19 epidemic has therefore led to a change in investors' perception of the valuation of equity markets, which then seemed overvalued in view of the potential risks generated by the pandemic.

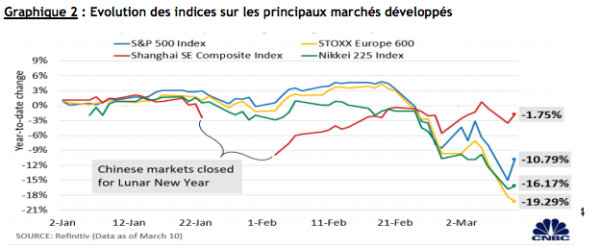

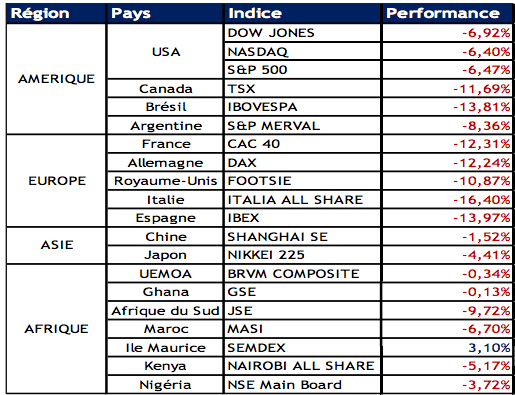

In addition, since the beginning of the week of March 9, 2020, a new milestone has been reached. On the one hand, the disagreement mentioned above between Russia and OPEC members over a drop in oil production has led to a drop in crude oil prices of nearly 27%. On the other hand, the decision taken on March 11 by the President of the United States, Donald Trump, to prohibit for a period of thirty (30) days, the entry into the United States to travelers from Europe, has led to a new black day on stock exchanges around the world. Thus Wall Street opened in sharp fall requiring a suspension of 15 minutes. European stock exchanges also suffered, with markets anticipating the impact of the ban on different sectors of the economy. The table below summarizes the performance of the stock markets during the session of March 12, 2020.

Table 1: Evolution of global stock markets during the session of March 12, 2020

A significant number of indices, particularly in Europe, have recorded double-digit falls. Thus the CAC 40 experienced its biggest ever fall on a session with a plunge in the index of 12.3%. During this black day, 31 of the values composing the CAC 40 fell by more than 10%. Not surprisingly, cyclical stocks have been sanctioned by investors. Thus, the list of the largest declines includes Renault (-21.9%), PSA (-18%) and VINCI (-17%). The European airline sector also fell sharply, with Norwegian shares collapsing by 24.9%. In addition, African stock exchanges, particularly those in Johannesburg and Casablanca, are already showing some negative impacts of the coronavirus on their developments, with declines of 9.72% and 6.7% respectively.

Evolution of the WAEMU Regional Stock Exchange (BRVM)

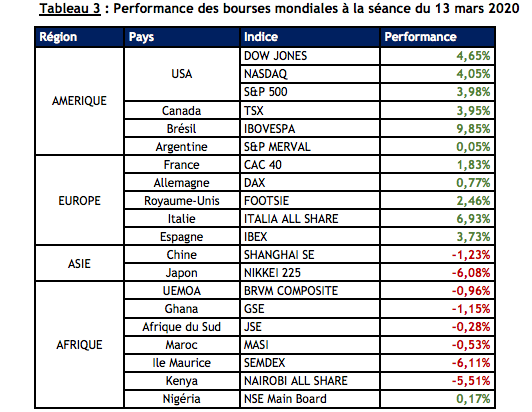

From the beginning of 2020 until March 3, the BRVM 10 and BRVM Composite indices recorded negative returns of -7.85% and -7.6% respectively. During the week of 09 to 13 March 2020, equity market indices showed slight declines. Thus, the BRVM 10 index fell by 0.86% while the BRVM Composite index fell 0.96%. Given the global stock market environment, these performances are proving to be relatively good.

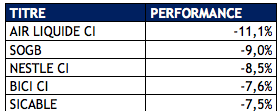

Table 2: Largest declines for the week of March 9 to 13, 2020 (Top 5)

It appears that of the five (5) shares that have fallen the most, three (3) are subsidiaries of major international groups, including: Air Liquide CI, Nestlé CI and BICI CI. The declines could be interpreted as anticipated consequences of the slowdown in international trade. In Paris, Air Liquide, Nestlé SA and BNP Paribas shares fell by 14.56%, 11.01% and 17.62% respectively over the week of 9 to 13 March 2020. Regarding the decline in SOGB shares, this would probably be related to the decline in palm oil and natural rubber prices. These agricultural products are suffering from the prospect of a contraction in Chinese consumption, which accounts for a significant share of global demand. On the other hand, for the SICABLE share, the decline in the price is mainly due to the publication of financial results down 16.4% in 2019 compared to the previous year.

conclusion

The situation is to be followed in the coming days, but already, the measures taken by the various public authorities (confinement, travel restrictions, closure of schools and universities, etc.) have given a little color to the Stock Exchanges.

Notes

1-OECD Economic Outlook, Interim Report, Coronavirus: The Global Economy under Threat, March 2020

2 - As a producer of intermediate goods, particularly in it, electronics, pharmaceuticals and >

transport equipment,

3 -As the world's largest buyer of raw materials.

4 -Chinese tourists account for about one-tenth of all international visitors in the world.

5 - According to WHO estimates, the SARS epidemic, which lasted 6 months, would have cost some 54 billion dollars (41 billion euros). One

figure that includes the fall in tourism revenues (-80% in China), as well as a shortfall of around 50% for companies

airlines, restaurants, tourist agencies and taxi drivers.

6- The forecasts for the United Kingdom and the euro area are based on the assumption of a basic trade agreement for trade in goods

effective early 2021.

-7 Waemu foreign trade report in 2018.

Vous devez être membre pour ajouter un commentaire.

Vous êtes déjà membre ?

Connectez-vous

Pas encore membre ?

Devenez membre gratuitement

24/06/2026 - Information générale

23/06/2026 - Information générale

22/06/2026 - Information générale

19/06/2026 - Information générale

18/06/2026 - Information générale

17/06/2026 - Information générale

17/06/2026 - Information générale

16/06/2026 - Information générale

15/06/2026 - Information générale

24/06/2026 - Information générale

23/06/2026 - Information générale

22/06/2026 - Information générale